Contactless Payments Continued: Benefits and drawbacks

Money has been around for thousands of years and has often been at or near the center of society. While money as a general concept has been around for a long time, both our cash and how we make payments have evolved, especially over the last few centuries. For example, floating fiat currencies are the norm now, while in the past, many currencies were pegged to a commodity, such as gold. Likewise, personal checks were quite popular just thirty years ago, but now, many businesses refuse to accept them. Instead, many sellers (and customers) prefer debit and credit cards.

Even payment cards may someday go the way of the personal check. Just as customers set aside cash in favor of cards, some consumers are skipping cards in favor of contactless payment methods, which eschew physical touch. Instead, simply wave a compatible device, such as a smartphone with an NFC chip, near a terminal and it’ll automatically connect so you can complete your payment via an app. Some credit and debit cards also offer contactless payment functionality.

COVID Coincidence and Adoption

Contactless payment offers a lot of convenience for both customers and businesses. Consumers were lured in by the low-friction functionality contactless offers during the COVID-19 pandemic. COVID fueled adoption as we were all were trying to maintain social distancing; contactless payments reduced touching of germ-covered terminals and cards. Yet even as the crisis subsided many people have continued to use contact-free payment methods.

Unfortunately, there are some drawbacks, or at least concerns, with contactless payment methods. Fraudsters are working to steal payment data and other valuable bits of info. Lost or stolen devices, meanwhile, could lead to unauthorized purchases and thus chargebacks and other issues. Other risks abound. That’s why we’re going to take a deeper look at contactless payments.

Contactless Payments are on the Rise, Thus Increasing Risks

Contactless payments represent a special risk for merchants as the technology is new. As a result, merchants are less familiar with the tech and also the processes involved. This can create knowledge and security gaps that fraudsters will exploit. As contactless payments become more popular, risks will increase.

Some payment stats and facts to consider:

- In 2019, only about a quarter of Americans had made at least one contactless payment. By May 2021, roughly 80 percent of Americans were using contactless payment.

- Nearly 60 percent reported that they would be more likely to shop at a retailer that offers such payment methods.

- In 2016, roughly 30 percent of consumer transactions were made with cash, according to the Federal Reserve. By 2021, this had dropped to just 20 percent.

- Credit and debit cards remain the most popular alternatives to cash, accounting for nearly 60 percent of all transactions (2021).

- Mobile app payment methods have risen from zero (2016) to 3 percent (2021), and “other” payment methods have risen to about 10 percent.

- As contactless payment becomes more popular, merchants need to learn how to handle them and mitigate risks. Understanding how such payment methods work offers a great first step.

How Does Contactless Payment Work?

So how do contactless payment methods work? Currently, most technologies use radio-frequency identification (RFID) or Near Field Communication (NFC) chips, which can communicate with nearby terminals (assuming they are compatible). Let’s take a look at the transaction process step-by-step.

- First, the user taps their contactless device near the contactless payment terminal. Technically, touch is not needed, the device simply needs to be near the terminal. If you see signs asking you to tap while checking out, it’s probably an NFC or RFID terminal.

- The RFID/NFC chip communicates with the terminal over encrypted radio frequencies.

- Once connected, the purchaser can quickly complete a payment via an app. There’s no need to dig out a card, mess around with cash, or write checks. Customers can simply tap and go.

- The business will receive the funds. By reducing friction and making payment easier, businesses may also increase sales and customer satisfaction.

Unfortunately, contactless payments have attracted scammers who try to steal money and data from buyers and sellers alike. While contact-free payments are convenient for many, they may also give rise to certain types of fraud. Sadly, many merchants end up hit with chargebacks stemming from fraud, and as a result, financial costs can quickly add up.

Contactless Payments and Chargebacks

Contactless payments, like other methods, can be used by criminals to perpetrate fraud. Often, fraudulent activities result in chargebacks for merchants. Simply put, a chargeback is an unauthorized refund. If a customer files a chargeback and their card issuing bank approves it, the payment made to a merchant will essentially be reversed and the funds will be sent back to the cardholder.

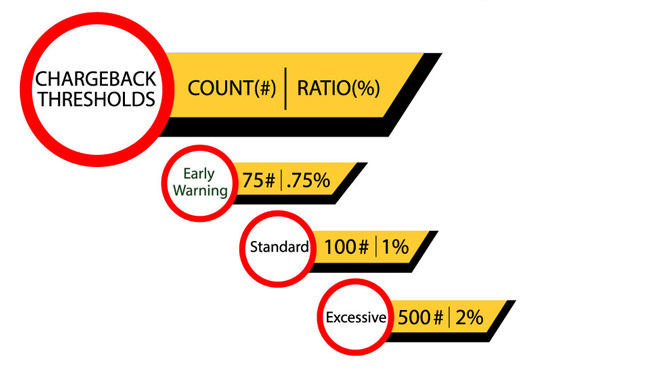

Chargebacks can cost merchants the revenues generated by a transaction. Additionally, the merchant will also have to pay a chargeback fee, which typically costs between $20 to $100. If a business gets hit with too many chargebacks, payment processors may start to charge them higher processing fees or they might even flat-out refuse to work with the merchant.

Many different fraudulent activities and disputes with customers can give rise to chargebacks, not just contactless payment methods. Still, with this payment method being somewhat new and less familiar to many merchants, it’s wise to be extra vigilant.

The good news is, contactless payment fraud isn’t as common as credit card fraud (yet). As of 2021, contactless payment fraud occurred at only about half of the rate of card fraud. However, criminals are finding some success hacking contactless payment. Chargebacks and other issues stemming from these new payment methods will likely rise in the future.

Payment Limits Mitigate Some but Not All Risks

Many authorities limit the size of purchases that can be made with contactless payments. This should, in theory, help mitigate fraud by making it more difficult for criminals to make off with expensive products and/or large amounts of cash. That said, many merchants are still racking up large losses from fraud with contactless payment methods. Below, you can see some of the current payment limits.

Contactless Payment Limits

- United States- $200

- Canada- $250 CAD

- Netherlands- €50

- United Kingdom- £100

- Japan- ¥20,000 JPY

- Australia- $200 AUD

As you can see, payments are typically limited to a few hundred dollars. This should help retailers avoid big-ticket fraud, at least with contactless payments. That said, scammers might get around the limits by running up numerous small transactions. Once chargeback fees and other costs are added up, even a small fraud case can easily cost a retailer hundreds of dollars.

What’s more, payment limits have been trending up. In the United Kingdom, for example, the max payment was lifted from £45 to £100. As payment limits rise, fraudsters could make off with more ill-gotten gains.

The Mechanics of Contactless Payment Fraud and How to Combat Chargebacks

For right now, probably the most common way to perpetuate contactless payment fraud is to steal someone’s phone or device. If the device isn’t protected with a password or the criminal otherwise gets into the phone, they can use it to make fraudulent contactless purchases. Depending on local laws and company policies, merchants may be able to ask for ID. However, the added friction could drive customers away.

There are steps merchants can take to reduce the risks of contactless payment fraud, including:

- Training employees to watch for suspicious shoppers.

- Setting up security cameras and letting potential fraudsters know that they’re being recorded to discourage criminal activity.

- Watching for skimmers, especially on self-service terminals such as gas station pumps and self-checkout aisles at grocery stores, where the payment terminal is not under constant live surveillance.

Make Sure You Have Clear Billing Descriptors

Intentional fraud is a major risk but non-criminal activities can also result in chargebacks and other problems. Fortunately, retailers can protect themselves here as well. Let’s look at how unclear billing descriptors can lead to chargebacks.

When a customer pays for something with a card or contactless device, it will eventually show up on their statement. The charge will be accompanied by a billing descriptor, which ideally will be very clear so that when the customer will recognize the charge.

Unfortunately, some businesses use vague descriptors. Let’s say John Doe owns the Smallville Gas Station and he uses a holding company named JD Holdings. After a customer pays the gas station, the charge shows up on their account as “JD Holdings,” and thus they might not recognize the charge. As a result, they might file a chargeback.

In the past, when most transactions were cash, billing descriptors weren’t quite as important. If a customer gives John Doe $20 in cash for gas there’s likely not going to be a mistaken identity dispute later on. The transaction has already been settled, and since it was settled in cash, there was a clear exchange of money and goods/services.

With more payments happening online or with the quick touch of a phone or other device, it’s harder for customers to track transactions. Clear billing descriptors reduce confusion.

Data is Your Friend

Retailers can gather data, including where the transaction took place and what was involved, which in turn could clear up confusion or help prove that a transaction was legitimate. With chargeback alerts offered via a dispute management platform, it’s possible to automatically gather and send data to banks before a chargeback is filed. The bank can then try to verify the transaction and clear up miscommunication.

Perhaps Jane Smith lives in Miami but a charge from a gas station in Washington appears on her debit or credit card statement. The payment was made with Jane’s NFC-enabled credit card but she hasn’t been to Washington recently. There’s a high chance that the charge was fraudulent. If the credit card transaction instead happened in Miami, it’s more likely that she made the purchase. On the other hand, if Jane lost her NFC-enabled smartphone in Miami, the criminal who found it try to use it very quickly.

With data from a dispute management platform in hand, banks will have an easier time verifying if there’s good cause to file for a chargeback. A charge from Washington may quickly lead to a chargeback. A charge in Miami might be further investigated and verified as legitimate before the chargeback is filed.

Ultimately, every business should closely examine any potential sources of chargebacks, no matter the payment method. Then, they should draw up plans to mitigate them when and where possible.

Contactless Payments Present Some Risks but also Many Opportunities

Can you simply ignore contactless payment methods? Doing so might prevent a few cases of fraud. However, you’ll also likely miss out on sales as NFC and RFID payment methods become more popular. With proactive crime prevention policies and the right tools, you can reduce the risk of contactless payment fraud and chargebacks while also catering to your customers and their preferences.