Visa Verifi’s RDR and CDRN Tools Explained

All industries are intensely competitive, and companies are frequently fighting to protect narrow profit margins and ever-tenuous market share. Chargebacks and fraud can be major threats for businesses big and small. They can result in chargeback fees, increased processing costs, lost inventory, and more. Fortunately, Verifi, a Visa solution, offers a variety of tools that merchants can use to prevent chargebacks, including Rapid Dispute Resolution and the Cardholder Dispute Resolution Network.

Did you know that all Verifi and Visa dispute solutions are available through ChargebackHelp? This makes us a one-stop-shop for all merchant chargeback prevention needs!

Before we dive into how Rapid Dispute Resolution (RDR) and the Cardholder Dispute Resolution Network (CDRN®) work, let’s go over why preventing chargebacks is crucial.

Preventing Chargebacks Protects the Merchant’s Chargeback Ratio

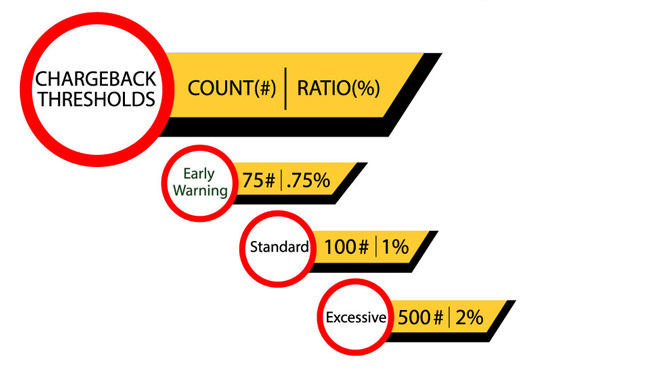

For sellers, chargeback ratios are one of the most important metrics to keep an eye on. A chargeback ratio is calculated as a percentage of transactions. So, a 1% chargeback ratio means that 1% of transactions within a given month result in chargebacks. High chargeback ratios can result in extra penalties levied by acquiring banks and Visa (and other card networks) and the merchant may be placed in the Visa Dispute Monitoring Program (VDMP) which is soon to be replaced by the Visa Acquirer Monitoring Program (VAMP) in Europe.

For Visa, if a merchant is hit with 100 or more chargebacks per month and their chargeback ratio hits or exceeds .9%, they will be placed in the Visa Dispute Monitoring Program (VDMP) and will have to contend with increased penalties. If the chargeback ratio hits or exceeds 1.8% and the merchant incurs more than 1,000 chargebacks in a month, the merchant can be placed in the Excessive VDMP, which results in even higher penalties. Chargeback ratios are calculated by individual card networks. So, chargebacks incurred with Visa credit cards will not impact the chargeback ratio computed by Mastercard.

Besides card networks, acquiring banks may also levy penalties if a merchant is hit with a lot of chargebacks. In some cases, the acquiring bank will refuse outright to work with merchants who are hit with a lot of chargebacks. Fortunately, Visa offers powerful tools for warding off chargebacks, including Rapid Dispute Resolution (RDR) and the Cardholder Dispute Resolution Network. These tools help merchants safeguard their chargeback ratio, enabling them to avoid penalties and placement in a monitoring program.

A Closer Look at RDR and CDRN

Both RDR and CDRN focus on preventing chargebacks. This is crucial because once a chargeback is filed, the seller will have to pay chargeback fees and their chargeback ratio will rise. With chargebacks, prevention is the best course. Fortunately, Rapid Dispute Resolution (RDR) and the Cardholder Dispute Resolution Network (CDRN), among other tools, can prevent chargebacks.

Let’s take a closer look at how these products can help. After that, we’ll cover some tips to make Visa’s tools easier to use.

Verifi Rapid Dispute Resolution Explained

Managing chargebacks can eat up a lot of labor. Fortunately, some powerful chargeback prevention tools automate and streamline various tasks, thus easing burdens on the business and its employees. Many merchants use Rapid Dispute Resolution (RDR) to quickly and automatically resolve disputes before a chargeback is filed.

RDR centers around a decision engine that automatically analyzes disputes in the pre-chargeback stage. Merchants can program the engine to follow specific rules. If a transaction meets the outlined rules, it is automatically resolved, and a message is sent to both acquiring and issuing banks to let them know that there’s no need to proceed with a chargeback. The acquiring bank will also send funds to the issuing bank, thus ending the dispute.

The RDR platform is quite flexible and powerful. Merchants can set various rules to filter transactions, including:

- Setting monetary thresholds- A merchant could decide to automatically resolve any transaction under a certain amount, say $25.

- Customer-Specific IDs- The RDR system can be set up to automatically resolve disputes for certain customers. For example, long-time customers in good standing can be automatically refunded. This helps ensure your more loyal customers stay happy and loyal.

- Product identifiers- Offer refunds for specific products. For example, if a brand of peanut butter was recalled, the seller can set the engine to automatically refund customers who bought the product and are now trying to get their money back.

- Specific Chargeback Reason Codes- Chargebacks classified into specified reason codes, such as charging a customer the incorrect amount, are refunded.

- Currency Codes- Transactions made with specific currencies are refunded. A resort in Mexico, for example, might set it so transactions in Canadian dollars are refunded.

The above list is not exhaustive. Also, merchants can set the decisioning system so that transactions must meet multiple criteria. For example, all European purchases below $20 could be refunded automatically. Currently, RDR works only for Visa transactions and the card issuer must be participating in the program. RDR is available globally and every Visa issuer can join the program.

Verifi Cardholder Dispute Resolution Network Explained

Like RDR, the Cardholder Dispute Resolution Network (CDRN) aims to prevent chargebacks before they become a black mark on the merchant’s record. CDRN doesn’t use a decisioning engine but does have other advantages. CDRN can be used globally not just with Visa cards but also with cards on other networks, such as Mastercard, American Express, and Discover. With CDRN, a merchant is given 72 hours to try to resolve the dispute before a chargeback is filed.

In a sense, the CDRN works by briefly freezing the chargeback. The merchant can then reach out to the cardholder to try to resolve the issue before a chargeback is filed. You might simply refund the customer, for example. If the chargeback occurred owing to poor billing descriptors or because the customer simply forgot about the purchase, a merchant may be able to resolve the dispute simply by jogging the customer’s mind.

Other Chargeback Mitigation Tools Offered by Verifi

While RDR and CDRN are powerful tools, they aren’t the only ones offered by Verifi. Order Insight provides detailed information to clear up confusion, such as forgotten purchases. Verifi INFORM, meanwhile, helps sellers gather data to analyze and model fraud. Data in hand, merchants can work to reduce fraudulent transactions. You can expect more chargeback mitigation tools to be rolled out in the future.

Does Mastercard Offer Similar Tools?

RDR is available only for Visa transactions. While the CDRN works with other card networks, including Mastercard, Discover, and American Express, Mastercard also offers its own unique tools through its subsidiary Ethoca.

Ethoca’s flagship chargeback prevention tool is Ethoca Alerts. These alerts work similarly to the alerts sent through Verifi’s CDRN platform. When a chargeback is requested, the issuer can pause the chargeback and communicate with the acquiring bank and merchant. Ethoca recommends merchants to resolve the dispute within 24 hours.

How ChargebackHelp Makes it Easier to Use Chargeback Prevention Tools

There are a few drawbacks to using chargeback alerts. Signing up for and setting up the tools can take quite a bit of effort. Further, since various companies offer different solutions, you’re left dealing with multiple vendors and the nuances of each. Once disputes start rolling in, trying to manage the various tools and use the many different platforms can feel like herding cats. You may find yourself constantly digging through manuals and forums.

That’s where ChargebackHelp comes in. With RESOLVE, you can manage both Visa/Verifi and Mastercard/Ethoca’s tools from one easy-to-use platform. We put ease of use at the core of our products, and as Verifi and Ethoca roll out evermore features, we strive to streamline processes and ensure that our users can maximize results by providing ongoing consultation based on years of experience.

Ultimately, a proactive approach to preventing and fighting chargebacks could make or break your company. Should a merchant fail to address chargebacks, their competitors could secure competitive advantages by keeping costs low with effective chargeback management. Further, with the right chargeback prevention tools, like RESOLVE, you can minimize the labor needed to successfully prevent chargebacks. This way, you can focus on growing your business.